Lab 6.5.2: Ridge Regression and the Lasso#

Attribution#

Orignal notebook by Emre Can (source). Updated to ISLRv2 by Daniel Kapitan (30-01-2022).

Introduction#

We will use Ridge, RidgeCV, Lasso and LassoCV from sklearn.linear_model to perform ridge regression and the lasso. We will do this in order to predict Salary on the Hitters data. We have already removed missing values upon loading the data from csv, but still need to transform qualitative variables into dummy variables. The latter is important because sklearn can only take numerical, quantitative inputs.

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from sklearn.linear_model import Ridge, RidgeCV, Lasso, LassoCV

from sklearn.metrics import mean_squared_error

from sklearn.model_selection import train_test_split

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import StandardScaler

%matplotlib inline

pd.set_option("display.max_rows", 20)

pd.set_option("display.max_columns", 12)

pd.set_option("display.float_format", "{:20,.5f}".format)

hitters = pd.read_csv("../datasets/Hitters.csv", index_col=0).dropna()

hitters.index.name = "Player"

X = hitters.drop(columns=['Salary'])

y = hitters.Salary

for col in ['League', 'Division', 'NewLeague']:

X[col] = pd.get_dummies(X[col]).iloc[:, 1]

Ridge Regression#

In sklearn the regularization parameter \(\lambda\) is named alpha, as is the case for the Ridge and RidgeCV classes. We choose to implement the function over a grid of values ranging from \(\lambda = 10^{10}\) to \(\lambda = 10^{-2}\), essentially covering the full range of scenarios from the null model containing only the intercept, to the least squares fit. As we will see, we can also compute model fits for a particular \(\lambda\) that is not one of the original grid values. Note that sklearn.linear_model does not standardize by default. To this purpose, we recommend to use StandardScaler as a preprocessing step in a Pipeline object.

Associated with each value of \(\lambda\) is a vector of ridge regression coefficients, stored in a matrix that can be accessed with the coef_ attribute. Because we are using a Pipeline, we need to specify the named step in the pipeline for which we want to access an attribute.

grid = 10 ** np.linspace(10, -2, 100)

ridge_model = make_pipeline(StandardScaler(with_mean=False), Ridge())

models = {}

for i, a in enumerate(grid):

ridge_model.set_params(ridge__alpha=a)

ridge_model.fit(X, y)

models[i] = {"alpha": a,

"coefs": ridge_model.named_steps["ridge"].coef_,

"intercept": ridge_model.named_steps["ridge"].intercept_,

}

models[49]

{'alpha': 11497.569953977356,

'coefs': array([ 3.49457396, 3.95273518, 2.98390005, 3.75468987, 3.9810762 ,

3.99185664, 3.46120924, 4.61714183, 4.84825026, 4.62598752,

4.9699381 , 5.0089575 , 4.27552715, -0.03422276, -1.87780156,

2.83798607, 0.23644179, -0.06961642, 0.04848929]),

'intercept': 453.4146479982648}

print(f"Number of models: {len(models)}")

print(f"Number of coefficients per model: {len(models[0]['coefs'])}")

Number of models: 100

Number of coefficients per model: 19

We expect the coefficient estimates to be much smaller, in terms of \(l_2\) norm, when a large value of \(\lambda\) is used, as compared to when a small value of \(\lambda\) is used. These are the coefficients when \(\lambda = 11,498\), along with their \(L_2\) norm:

def print_ridge_results(i):

print(f"alpha: {models[i]['alpha']}")

print(f"intercept: {models[i]['intercept']}")

print(pd.Series(models[i]['coefs'], index=X.columns))

print(f"L2: {np.sqrt(np.sum([x**2 for x in models[i]['coefs'] ]))}")

print_ridge_results(49)

alpha: 11497.569953977356

intercept: 453.4146479982648

AtBat 3.49457

Hits 3.95274

HmRun 2.98390

Runs 3.75469

RBI 3.98108

Walks 3.99186

Years 3.46121

CAtBat 4.61714

CHits 4.84825

CHmRun 4.62599

CRuns 4.96994

CRBI 5.00896

CWalks 4.27553

League -0.03422

Division -1.87780

PutOuts 2.83799

Assists 0.23644

Errors -0.06962

NewLeague 0.04849

dtype: float64

L2: 15.509329901628677

In contrast, here are the coefficients when \(\lambda = 705\), along with their \(l_2\) norm. Note the much larger \(l_2\) norm of the coefficients associated with this smaller value of \(\lambda\).

print_ridge_results(59)

alpha: 705.4802310718645

intercept: 106.26999409130377

AtBat 16.43691

Hits 24.14789

HmRun 11.54152

Runs 20.79688

RBI 19.99724

Walks 23.88545

Years 13.47874

CAtBat 22.48210

CHits 25.85029

CHmRun 23.99095

CRuns 26.45447

CRBI 26.81973

CWalks 18.86201

League 4.29467

Division -19.59863

PutOuts 24.64957

Assists 1.67757

Errors -2.60291

NewLeague 3.19072

dtype: float64

L2: 84.4107408389558

We now split the samples into a training set and a test set in order to estimate the test eroor of ridge regression and the lasso. There are various ways to randomly split a data set. The first is to produce a random vector of True, False elements and select the observations corresponding to True for the training data. The second is to randomly choose a subset of numbers between 1 and \(n\); these can then be used as the indices for the training observations. Another way is to use the train_test_split function from sklearn, which we demonstrate here.

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.5, random_state=1)

Next we fit a ridge regression model on the training set, and evaluate its MSE on the test set, using \(\lambda = 4\).

ridge2 = make_pipeline(StandardScaler(with_mean=False), Ridge(alpha=4))

ridge2_fit = ridge2.fit(X_train, y_train)

y_pred2 = ridge2.predict(X_test)

print(pd.Series(ridge2_fit.named_steps["ridge"].coef_, index=X.columns))

print("MSE:", mean_squared_error(y_test, y_pred2))

AtBat -210.80732

Hits 193.07693

HmRun -51.43737

Runs 1.62407

RBI 81.45892

Walks 94.58254

Years -28.02948

CAtBat -117.92436

CHits 91.15963

CHmRun 91.76201

CRuns 101.11545

CRBI 117.59896

CWalks -38.43468

League 35.79205

Division -60.24544

PutOuts 125.55607

Assists 25.55919

Errors -18.51890

NewLeague -18.65062

dtype: float64

MSE: 102144.52395076491

The test MSE is 102,144. Note that if we had instead simply fit a model with just an intercept, we would have predicted each test observation using the mean of the training observations. In that case, we could compute the test set MSE like this:

np.mean((np.mean(y_train) - y_test)**2)

172862.23592080915

We could also get the same result by fitting a ridge regression model with a very large value of \(\lambda\). Note that 1e10 means \(10^{10}\).

# very high lambda

ridge3 = make_pipeline(StandardScaler(with_mean=False), Ridge(alpha=1e10))

ridge3_fit = ridge3.fit(X_train, y_train)

y_pred3 = ridge3.predict(X_test)

print(pd.Series(ridge3_fit.named_steps["ridge"].coef_, index=X.columns))

print("MSE:", mean_squared_error(y_test, y_pred3))

AtBat 0.00000

Hits 0.00000

HmRun 0.00000

Runs 0.00000

RBI 0.00000

Walks 0.00000

Years 0.00000

CAtBat 0.00000

CHits 0.00000

CHmRun 0.00000

CRuns 0.00000

CRBI 0.00000

CWalks 0.00000

League -0.00000

Division -0.00000

PutOuts 0.00000

Assists -0.00000

Errors 0.00000

NewLeague -0.00000

dtype: float64

MSE: 172862.22059245987

So fitting a ridge regression model with \(\lambda = 4\) leads to a much lower test MSE than fitting a model with just an intercept. We now check whether there is any benefit to performing ridge regresion with \(\lambda = 4\) instead of just performing least squares regression. Recall that least squares is simply ridge regression with \(\lambda = 0\).

ridge4 = make_pipeline(StandardScaler(with_mean=False), Ridge(alpha=0))

ridge4_fit = ridge4.fit(X_train, y_train)

y_pred4 = ridge4.predict(X_test)

print(pd.Series(ridge4_fit.named_steps["ridge"].coef_, index=X.columns))

print("MSE:", mean_squared_error(y_test, y_pred4))

AtBat -266.55305

Hits 197.70622

HmRun -38.10318

Runs -1.00800

RBI 103.11985

Walks 79.75021

Years 45.35770

CAtBat -1,399.81138

CHits 1,426.95481

CHmRun 264.03798

CRuns 86.85878

CRBI -211.14239

CWalks 42.53360

League 66.82285

Division -56.87028

PutOuts 126.07556

Assists 65.81609

Errors -38.31389

NewLeague -40.96269

dtype: float64

MSE: 116690.4685666012

In general, instead of arbitrarily choosing \(\lambda = 4\), it would be better to use cross-validation to choose the tuning parameter \(\lambda\). We can do this using the built-in cross-validation function RidgeCV. By default, the function performs ten-fold cross-validation, though this can be changed using the argument cv.

ridge_cv = make_pipeline(

StandardScaler(with_mean=False),

RidgeCV(alphas=grid, scoring="neg_mean_squared_error"),

)

ridge_cv.fit(X_train, y_train)

ridge_cv.named_steps["ridgecv"].alpha_

75.64633275546291

Therefore, we see that the value of \(\lambda\) that results in the smallest cross-validation error is 75.6. What is the test MSE associated with this value of \(\lambda\)?

# cv_lambda

ridge5 = make_pipeline(

StandardScaler(with_mean=False), Ridge(alpha=ridge_cv.named_steps["ridgecv"].alpha_)

)

ridge5_fit = ridge5.fit(X_train, y_train)

y_pred5 = ridge5.predict(X_test)

print(pd.Series(ridge5_fit.named_steps["ridge"].coef_, index=X.columns))

print("MSE:", mean_squared_error(y_test, y_pred5))

AtBat -1.87522

Hits 40.04216

HmRun -2.25864

Runs 18.79162

RBI 34.08055

Walks 48.03307

Years 5.77862

CAtBat 15.43406

CHits 34.10274

CHmRun 45.40307

CRuns 34.78448

CRBI 45.19872

CWalks 24.57958

League 9.43059

Division -46.01926

PutOuts 83.78692

Assists -2.44659

Errors -1.98723

NewLeague 4.97471

dtype: float64

MSE: 99820.74305168974

This represents a further improvement over the test MSE that we got using \(\lambda = 4\). As expected, none of the coefficients are zero - ridge regression does not perform variable selection!

The Lasso#

We saw that ridge regression with a wise choice of \(\lambda\) can outperform least squares as well as the null model on the Hitters data set. We now ask whether the lasso can yield either a more accurate or a more interpretable model than ridge regression. In order to fit a lasso model, we use Lasso from sklearn. Other than that change, we proceed just as we dit in fitting a ridge model

lasso_model = make_pipeline(StandardScaler(with_mean=False), Lasso(max_iter=10_000))

lassos = {}

for i, a in enumerate(grid):

lasso_model.set_params(lasso__alpha=a)

lasso_model.fit(X, y)

lassos[i] = {

"alpha": a,

"coefs": lasso_model.named_steps["lasso"].coef_,

"intercept": lasso_model.named_steps["lasso"].intercept_,

}

ax = plt.gca()

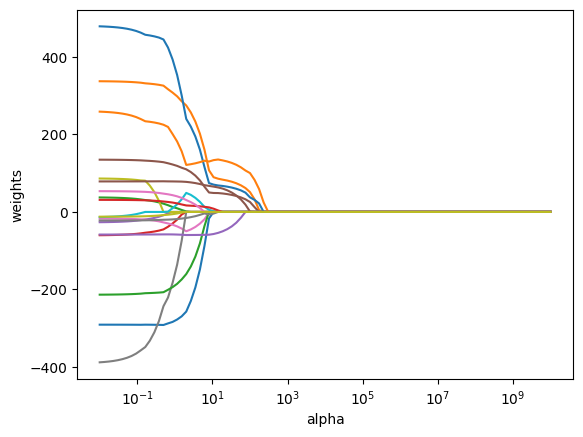

ax.plot(grid, [x['coefs'] for x in lassos.values()] )

ax.set_xscale("log")

plt.axis("tight")

plt.xlabel("alpha")

plt.ylabel("weights");

We can see from the coefficient plot that depending on the choice of tuning parameter, some of the coefficients will be exactly equal to zero. We now perform cross-validation and compute the associated test error.

lasso_cv = make_pipeline(

StandardScaler(with_mean=False),

LassoCV(alphas=grid, max_iter=10_000, cv=10),

)

lasso_cv.fit(X_train, y_train)

lasso_cv.named_steps["lassocv"].alpha_

24.77076355991714

lasso2 = lasso_model = make_pipeline(

StandardScaler(with_mean=False),

Lasso(alpha=lasso_cv.named_steps["lassocv"].alpha_, max_iter=10_000),

)

lasso2_fit = lasso2.fit(X_train, y_train)

y_pred2 = lasso2_fit.predict(X_test)

print(pd.Series(lasso2_fit.named_steps['lasso'].coef_, index=X.columns))

print("MSE:", mean_squared_error(y_test, y_pred2))

AtBat 0.00000

Hits 51.23005

HmRun 0.00000

Runs 0.00000

RBI 0.00000

Walks 67.81051

Years 0.00000

CAtBat 0.00000

CHits 0.00000

CHmRun 20.50906

CRuns 0.00000

CRBI 182.42795

CWalks 0.00000

League 0.00000

Division -47.16690

PutOuts 111.64058

Assists -0.00000

Errors -0.00000

NewLeague 0.00000

dtype: float64

MSE: 104808.76054941259

This is substantially lower that the test set MSE of the null model and of least squares, and very similar to the test MSE of ridge regression with \(\lambda\) chosen by cross-validation.

However, the lasso has a substantial advantage of ridge regression in that the resulting coefficients estimates are sparse. Here we see that 13 of the 19 coefficient estimates are exactly zero. So the lasso model with \(\lambda\) chosen by cross-validation contrains only 6 variables.